All Categories

Featured

Table of Contents

[/image][=video]

[/video]

Multi-year guaranteed annuities, likewise known as MYGAs, are repaired annuities that secure a stable rates of interest for a defined period. Surrender periods usually last three to ten years. Since MYGA rates transform daily, RetireGuide and its partners update the following tables below frequently. It is essential to inspect back for the most recent information.

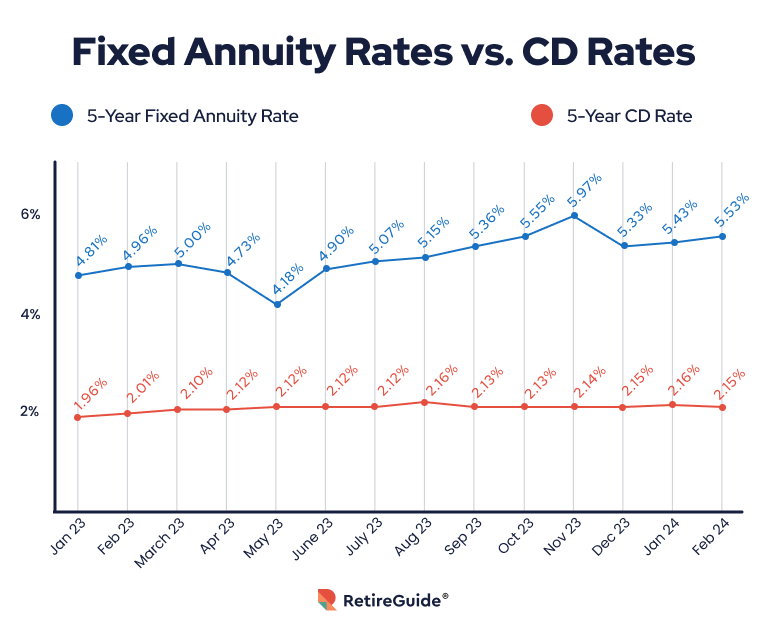

A number of elements establish the rate you'll get on an annuity. Annuity rates have a tendency to be higher when the basic degree of all passion prices is greater. When shopping for taken care of annuity rates, you may locate it helpful to compare rates to deposit slips (CDs), an additional preferred choice for secure, reliable development.

In general, fixed annuity rates surpass the rates for CDs of a comparable term. Other than making a greater price, a taken care of annuity could provide far better returns than a CD since annuities have the benefit of tax-deferred growth. This implies you will not pay taxes on the rate of interest made until you start obtaining payments from the annuity, unlike CD rate of interest, which is counted as gross income yearly it's gained.

This led many experts to think that the Fed would reduce prices in 2024. However, at a plan discussion forum in April 2024, Federal Reserve chair Jerome Powell suggested that rates might not come down for some time. Powell claimed that the Fed isn't certain when rate of interest price cuts may occur, as rising cost of living has yet to drop to the Fed's benchmark of 2%.

Hartford Variable Annuity

Keep in mind that the most effective annuity prices today might be different tomorrow. It is essential to check with insurance coverage business to verify their particular prices. Start with a cost-free annuity consultation to learn how annuities can help fund your retirement.: Clicking will take you to our companion Annuity.org. When contrasting annuity rates, it is necessary to conduct your very own research study and not entirely select an annuity merely for its high rate.

Take into consideration the kind of annuity. Each annuity type has a various variety of ordinary passion prices. For instance, a 4-year set annuity might have a greater rate than a 10-year multi-year ensured annuity (MYGA). This is since fixed annuities may supply a higher rate for the very first year and afterwards minimize the rate for the rest of the term, while MYGAs assure the rate for the entire term.

The warranty on an annuity is just as good as the business that issues it. If the business you acquire your annuity from goes broke or bust, you could shed cash. Examine a company's monetary stamina by speaking with nationally recognized impartial rating companies, like AM Ideal. A lot of experts suggest only taking into consideration insurance firms with a score of A- or above for long-lasting annuities.

Annuity earnings increases with the age of the buyer due to the fact that the earnings will be paid out in less years, according to the Social Protection Management. Don't be amazed if your price is higher or lower than another person's, also if it's the same product. Annuity prices are just one aspect to think about when buying an annuity.

Comprehend the costs you'll have to pay to provide your annuity and if you need to cash it out. Squandering can set you back approximately 10% of the value of your annuity, according to the Wisconsin Workplace of the Commissioner of Insurance policy. On the various other hand, management costs can accumulate with time.

Morningstar Annuity

Inflation Inflation can consume your annuity's value gradually. You might take into consideration an inflation-adjusted annuity that improves the payments gradually. Understand, though, that it will dramatically decrease your preliminary payments. This indicates less cash early in retired life but even more as you age. Take our free quiz & in 3 very easy actions.

Scan today's listings of the most effective Multi-year Guaranteed Annuities - MYGAs (updated Thursday, 2025-03-06). These checklists are sorted by the abandonment charge duration. We modify these checklists daily and there are regular modifications. Please bookmark this web page and come back to it typically. For professional assistance with multi-year ensured annuities call 800-872-6684 or click a 'Get My Quote' switch following to any kind of annuity in these checklists.

You'll likewise take pleasure in tax benefits that financial institution accounts and CDs do not provide. Yes. In many situations deferred annuities permit a total up to be taken out penalty-free. However, the allowed withdrawal amount can vary from company-to-company, so be certain to read the product pamphlet meticulously. Deferred annuities commonly allow either penalty-free withdrawals of your earned interest, or penalty-free withdrawals of 10% of your contract value every year.

The earlier in the annuity period, the higher the charge portion, described as surrender costs. That's one reason it's ideal to stick to the annuity, once you dedicate to it. You can take out whatever to reinvest it, yet prior to you do, make certain that you'll still triumph this way, also after you figure in the abandonment cost.

The surrender cost could be as high as 10% if you surrender your contract in the initial year. A surrender cost would be charged to any type of withdrawal higher than the penalty-free amount permitted by your deferred annuity contract.

Once you do, it's best to see it through throughout. You can establish up "systematic withdrawals" from your annuity. This means that the insurer will certainly send you settlements of rate of interest monthly, quarterly or annually. Using this method will not use your initial principal. Your various other alternative is to "annuitize" your postponed annuity.

No Load Variable Annuity

This opens up a selection of payment options, such as income over a single lifetime, joint lifetime, or for a given period of years. Several delayed annuities allow you to annuitize your contract after the first agreement year. A significant difference is in the tax treatment of these items. Rate of interest earned on CDs is taxable at the end of yearly (unless the CD is held within tax professional account like an individual retirement account).

The rate of interest is not tired till it is removed from the annuity. Simply put, your annuity expands tax obligation deferred and the rate of interest is worsened every year. Nonetheless, comparison buying is constantly an excellent idea. It's real that CDs are insured by the FDIC. MYGAs are guaranteed by the individual states normally, in the array of $100,000 to $500,000.

Chase Fixed Annuity Rates

Either you take your money in a lump sum, reinvest it in one more annuity, or you can annuitize your agreement, converting the lump sum right into a stream of income. By annuitizing, you will only pay tax obligations on the rate of interest you get in each repayment.

These attributes can differ from company-to-company, so make certain to explore your annuity's death benefit features. There are a number of advantages. 1. A MYGA can indicate lower tax obligations than a CD. With a CD, the interest you earn is taxable when you earn it, even though you do not receive it until the CD grows.

Not only that, but the compounding interest will be based on an amount that has actually not already been taxed. Your recipients will get the full account value as of the date you dieand no surrender costs will certainly be subtracted.

Your recipients can select either to get the payout in a swelling sum, or in a series of revenue payments. 3. Usually, when someone dies, even if he left a will, a judge determines that obtains what from the estate as sometimes loved ones will argue regarding what the will certainly methods.

It can be a long, complicated, and extremely expensive process. People most likely to excellent sizes to prevent it. With a multi-year set annuity, the owner has actually clearly designated a beneficiary, so no probate is required. The money goes straight to the recipient, no doubt asked. If you contribute to an IRA or a 401(k) plan, you receive tax deferral on the earnings, much like a MYGA.

{kind=link}

Latest Posts

Inherited Annuity 1035 Exchange

Which Is Better Ira Or Annuity

Nationwide New Heights Annuity